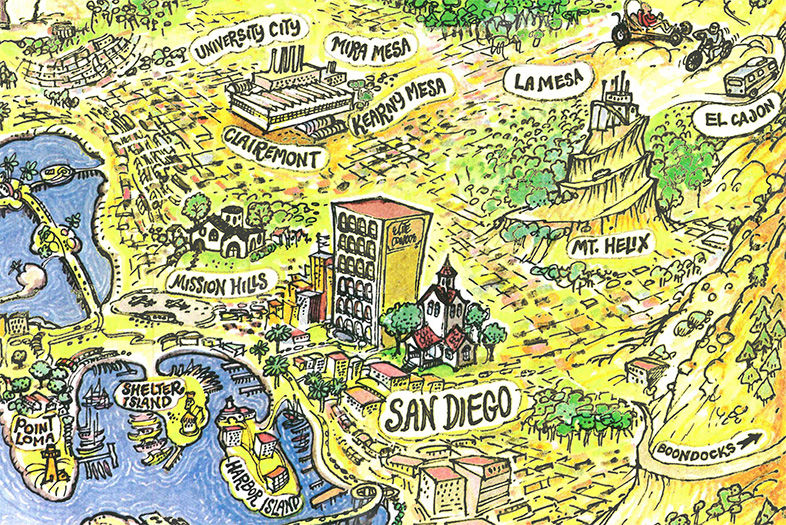

Complaining about how much easier past generations had it—no smartphones to distract us, no high-fructose corn syrup to poison us—is a beloved pastime. But when it comes to buying a home in San Diego, little has changed.

In a 1977 San Diego Magazine article titled “Are You Living Where You Should?” writer Bill Ritter examines the county’s housing market in the era of disco and Jimmy Carter—and some of his takeaways sound awfully familiar.

“Despite the wide variety [of home styles], there is not a limitless supply of either homes or land to build on them,” he writes. “And the situation can only get tighter as more and more people from across the country and in other parts of California eye San Diego’s excellent climate and aesthetically pleasing topography.”

New residential building permits were down 20 percent in 2017, according to the Building Industry Association of San Diego County. And just like our real estate experts say about our current milieu, the mantra even then was “Buy now!”

In his piece, Ritter scans for the top real estate pockets. He suggests buying in “older sections,” like Mission Hills and Hillcrest, that off er “urban life in a near-rural setting.” Back then, houses in those neighborhoods averaged $68,000 and $40,000, respectively. Now? Try million-dollar price tags.

As has always been the case, living by the beach will cost you. In 1977 La Jolla, the average price for a new home was $120,000, while moving inland to Clairemont and Tierrasanta dramatically dropped prices to about $40,000.

Ritter goes on to claim that South Bay is “where the action is,” citing that in early 1976, 16 developments went from selling 24 to nearly 50 units per week. Today, the trend continues; all eyes are on Otay Mesa’s new Millenia development, with apartments, for-sale homes, 80 walkable city blocks, restaurants, shops, and more.

What also caught our eye from Ritter’s reporting were the reasons for the ’70s housing market shift. For starters, only 15 percent of San Diegans were able to afford a home on one salary, so more women had to enter the workforce, which “changed the home buying picture.” Then there’s the reason nearly every generation can attest to: a tight economy. In 1977, nearly 75 percent of American families couldn’t afford to buy a new home. Today, more than 38 million American households can’t afford their housing, an increase of 146 percent in the past 16 years, according to a 2017 Harvard University study. It’s no wonder the title of this article was a question—one we continue to ask 30 years later.

From the Archives: San Diego’s Real Estate Market in 1977

Guides

JULY 6, 2026

6 Perfect Days in North County

We found a handful of inspiring people who live in, and truly know, these 'hoods and asked them how they’d spend their time out and about

Growing up in Carlsbad, I never quite understood why people vacationed there. What, so you want to check out the field where I have soccer practice? Pay my orthodontist a visit? Carlsbad just felt like a town by the beach, no better or worse than any other in the country. It took going to college out of state for me to actually understand just how rare a place like Carlsbad is.

Thanksgiving break my freshman year, my first time coming home after three months in the Midwest, my shoulders dropped. I rolled down the windows and drove to lifeguard tower 37—the hangout magnet for Carlsbad’s youths (and, in the summer, tourists)—and the smells of the ocean woke me right up like smelling salts do. I finally got it.

Carlsbad isn’t just a stopover town on your way to something better. It is the destination. Travel + Leisure named Carlsbad one of the top 50 places around the world to travel in 2026. From the whole globe, the travel magazine picked my home. Sure, we’ve got the Flower Fields and Legoland—but now it’s the smaller ships and indier dreams that are giving it street-level character.

It’s not just Carlsbad, either. People have talked about the “North County bubble” for decades—a force field that prevents its residents from traveling south of the 56. It’s often used derogatorily, and it’s a fairly accurate burn.

For decades, living up in North County meant giving up on culture, or at least culture within close proximity. But now, the main expansion of San Diego culture is happening up north. Central San Diego restaurants have started taking notice and are expanding into the area—spurred no doubt by Oceanside’s food boom and the Jeune et Jolie–Campfire–Wildland–Lilo constellation in Carlsbad. City Heights burger joint Key & Cleaver opened a new spot in Oceanside; the owners of Parc Bistro-Brasserie in Bankers Hill opened Parc Lounge in Rancho Santa Fe. Possibly the strongest market indicator is that Sam Fox—one of the most successful restaurateurs west of the Rockies—has started focusing on North County for his concepts. In 2025, he opened both The Henry in Carlsbad and Culinary Dropout in Del Mar.

For the ultimate insider guide, we found a handful of inspiring people who live and create and truly know six North County neighborhoods—San Marcos, Escondido, Oceanside, Leucadia, Rancho Santa Fe, and Vista—and asked them how they’d spend a dream day out and about in their town.

Courtesy of North City Farmers Market

San Marcos

San Marcos is in full renaissance mode. The biggest story is that the grand North City vision is starting to peek through the scaffolding. It’s essentially the North County Downtown that’s been written in the tea leaves and discussed whenever someone gets stuck in traffic at the 5/805 merge: a 200-acre, pedestrian-friendly, mixed-use face-changer that’s slated for 2,600 homes, 350,000 square feet of retail and restaurants, 250 hotel rooms, and about a million square feet of offices and labs. Its most recent manifestation is 222 North City—a 12-story residential tower with over 450 residences, rooftop garden, pool cabanas, art installations, and almost 20,000 square feet of ground-floor retail (Necessity Coffee, Buona Forchetta, Draft Republic, Milonga Empanadas, and a grocery store anchor on its way).

Which means Restaurant Row is no longer burdened with being the primary caregiver for the hungry or the socially inclined. Patricia Prado-Olmos has watched the city morph during her nearly three-decade tenure at CSUSM, having spent the past six years as the school’s chief community engagement officer. She also just announced her forthcoming retirement at the end of the 2026–2027 school year, so she’ll have even more time to haunt local haunts.

Meet the Local: Patricia Prado-Olmos

Those in the know call the university “Cal State StairMaster” from the Sisyphean amount of stairs on the hillside campus. So, any day at or around CSUSM should start with a homestyle carbo-load (biscuits and gravy) from Mama Kat’s.

“There’s something about this breakfast spot that immediately puts me in a good mood,” she says. Mama Kat’s is also known for its pie (strawberry-rhubarb), which is breakfast if you change your perspective.

After a few hours on campus—with a break to pet the university’s official therapy goldendoodle, Frank, who helps ease finals tremors or apprehension of on-campus stairs—Prado-Olmos will wander into North City, just steps away. She says the almond croissant and coffee at Christophe Rull Patisserie rival Parisian cafés: “It feels like the kind of place you’d stumble across in a much bigger city.”

Rull, a Michelin-trained pastry chef who’s done stints on Netflix (Bake Squad) and Food Network (Super Mega Cakes, Halloween Wars), opened his patisserie last fall. The hype hasn’t cooled off yet: Get there early because the crowds do.

Emma Veidt is an editor at San Diego Magazine. She earned her bachelor's and master's degrees from the Missouri School of Journalism. She loves running, hiking, and rock climbing, but really, she mostly loves encounters with the street cats around North Park.

Just south of Lake Hodges near 4S Ranch and Poway, Rancho Bernardo is a suburban community that blends residential neighborhoods with industrial pockets, elevated by a decidedly diverse food scene.

Over 60 years ago, this North County neighborhood was once part of a family ranch. Since that time, big tech companies have taken up residence here, including Amazon, Sony Electronics, Oura Ring, HP, Teradata, and ASML. Rancho Bernardo Inn serves as a community hub, with locals frequently meeting at the hotel’s restaurants, golf course, and spa.

Whether it’s work or a round of golf that brings you to Rancho Bernardo, we’ve taken care of the agenda planning with our guide to the area’s best restaurants, activities, and shops.

Courtesy of Avant Restaurant

Rancho Bernardo Restaurants, Bars, and Coffee Shops

Avant

Sample ingredients plucked straight from Rancho Bernardo Inn’s onsite garden and served at their signature restaurant Avant. One of the neighborhood’s most upscale dining options, they serve a French-inspired menu with nods to California, including many seafood options. Don’t miss their more casual sister restaurant Veranda for al fresco dining.

Wood-fired pizzas and handmade pastas are standouts at The Kitchen, Bernardo Winery’s counter-service restaurant specializing in Sicilian flavors. Charcuterie boards and bruschetta make for great starters or snacks while wine tasting.

13330 Paseo Del Verano Norte

Bushfire Kitchen

Fast-casual and family-owned eatery Bushfire Kitchen recently opened a location in Rancho Bernardo, serving sandwiches, bowls, salads, burgers, protein plates, and housemade empanadas. Bushfire prepares comfort food with healthy ingredients, and offers plenty of vegetarian and vegan options.

11962 Bernardo Plaza Drive, Suite 110

The Cork & Craft

Some might call The Cork & Craft an overachiever. This gastropub has an in-house craft brewery and winery: Abnormal Beer and Wine. The more, the merrier. Their sushi menu is definitely worth exploring, but don’t miss other specialties like garlic noodles, chicken wings, and pork belly.

16990 Via Tazon

Courtesy of Carvers Steaks & Chops

Carvers Steaks & Chops

You don’t have to leave Rancho Bernardo to get a white tablecloth steakhouse experience. Carvers Steaks & Chops has prime rib (their best seller), filet, ribeye, porterhouse, New York strip, and other cuts, served alongside crab-stuffed mushrooms, wedge salad, French onion soup, potato skins, and other steakhouse specialties.

1940 Bernardo Plaza Drive

Burma Place

This no-frills Burmese restaurant is known for its traditional tea leaf salad that’s topped with sesame and sunflower seeds, garlic chips, peanuts, tomatoes, jalapeños, fried yellow beans, and fermented green tea leaf dressing. Tucked into a nondescript strip mall, Burma Place is a great takeout option when you want to eat garlic noodles, fried rice, chicken curry, and samosas from the comfort of your couch.

16719 Bernardo Center Drive, Suite A

Phở Ca Dao

Find authentic Vietnamese cuisine at Phở Ca Dao, including favorites like phở noodle soup, vermicelli noodles, broken rice dishes, and spring rolls. One of eight locations throughout San Diego, this family-owned chain uses robot servers for food delivery.

11808 Rancho Bernardo Road, Suite 100

The Kebab Shop

It’s all about the sauce at fast-casual Mediterranean restaurant The Kebab Shop. Smothering your chicken shawarma, gyro, or falafels in garlic yogurt, cilantro jalapeno, fire chili, and dill yogurt sauce is practically a rite of passage. The hardest part is deciding whether to order a wrap, bowl, or salad.

11980 Bernardo Plaza Drive

Casa Lahori

Get a taste of South Asian flavors at Casa Lahori, a Pakistani restaurant noted for its grilled meat kabobs. Other best-selling dishes include beef nihari, chicken biryani, and shahi paneer— best enjoyed with naan bread.

11975 Bernardo Plaza Drive

Kangnam Korean BBQ

Grill your own meat on the tabletop at Kangnam Korean BBQ, an interactive, all-you-can-eat experience that’s well-suited for large groups. Marinated beef bulgogi, grilled galbi short ribs, and spicy pork are served alongside traditional banchan dishes like kimchi, japchae glass noodles, and flavorful stews. Weekday lunch specials provide a nice discount on these filling meals.

11828 Rancho Bernardo Road, Suite 117–119

Courtesy of Curry & More Indian Bistro

Curry & More Indian Bistro

Dig in to your favorite curries and kebabs at Curry & More Indian Bistro. Most entrees are served with a choice of two side dishes, including basmati rice, potatoes with cumin, daal, naan, or mixed greens. Help offset the spice with one of their sweet mango or strawberry lassi drinks.

Kai Oliver-Kurtin is a San Diego-based writer who covers travel, dining, events, and culture. Her writing has been published in USA Today, Condé Nast Traveler, Fodor's Travel, Marie Claire, and HuffPost, among others.

Some keep lists of favorite books, of quotes, of enemies whose time shall come. At SDM we keep vast, nuanced, hotly debated lists of the best food and drink in the city. Menus are our smut novels. From Michelin stars to mom and pops, our list constantly evolves over hundreds of new bites tried every year. Here’s the 2026 list from food critic Troy Johnson and 129,000-plus votes from our readers, who really, really know their food.

Scroll down for the full list of Best Restaurant winners

Troy Johnson is the magazine’s award-winning food writer and humorist, and a long-standing expert on Food Network. His work has been featured on NatGeo, Travel Channel, NPR, and in Food Matters, a textbook of the best American food writing.

Renewable energy companies building hundreds of power plants. Biotech startups using artificial intelligence to create personalized medicine for children with rare diseases. Hospitality companies quietly powering thousands of local events. Consumer brands growing from beach-town startups into national businesses. These are the kinds of companies driving San Diego’s economy today, and the businesses recognized at this year’s San Diego Business Impact Awards offer a snapshot of where the region is headed.

Hosted July 23 by San Diego Regional Economic Development Corporation (EDC) and JPMorganChase, the second annual awards event honored four local companies for innovation, growth, and economic impact. More than 100 nominations from San Diego’s middle-market businesses were reviewed by a 10-person judging committee, with winners selected across four categories: startup, early-stage innovator, rising star, and established heavyweight.

Two-time honoree Jimbo Someck, founder of Jimbo’s organic grocery stores, also joined the event for a fireside chat on buying local, supporting emerging brands, and giving back to the community.

“San Diego’s strength comes from its makers and builders—the resilient people who endure great risks and overcome obstacles to build and scale a company,” says Aaron Ryan, San Diego Region Manager and Middle Market Banking at JPMorganChase & Co. “These awards aren’t just recognition; they spotlight the talent, grit, and innovation shaping our region’s future. By celebrating those who create and build, we foster connections and fuel the growth that keeps San Diego thriving.”

Photo Credit: Matt Furman

Building the Infrastructure Behind Clean Energy

Heavyweight honoree SOLV Energy has grown alongside the country’s rapid investment in renewable power. “It’s an exciting time for SOLV Energy as we are experiencing significant growth,” says CEO George Hershman. “The business has doubled over the last year and has almost double-digit growth since its inception.”

The Rancho Bernardo-based company designs, builds, operates, and maintains utility-scale solar and energy storage facilities. Since its founding in 2008, SOLV Energy has built more than 500 power plants.

Growth has translated directly into hiring. About 200 employees work from the company’s local headquarters, including roughly 20 interns. “Our intern program is a big part of the way that we grow our workforce,” Hershman says. “Last year, 43 percent of our interns became full-time employees. We believe San Diego is a great community to build and grow a high-tech infrastructure and technology company because of the incredible workforce—the ability to attract top talent and draw from world-class universities.”

Photo Credit: Matt Furman

Developing Medicine One Patient at a Time

Startup honoree La Jolla Labs is tackling one of medicine’s biggest challenges by developing personalized RNA therapeutics for patients with rare diseases—many of them children with neurological disorders like ALS. Using proprietary artificial intelligence and machine learning tools, the biotech company develops treatments tailored to each patient’s specific genetic mutation.

CEO Tamar Grossman says the recognition reflects how far the company has come despite limited resources. “We’re honored to be recognized for our ability to change and save patients’ lives and turn our lean startup into a clinical company with very minimal resources,” she says.

Grossman credits San Diego’s concentration of research institutions—including UC San Diego, the Salk Institute, and Scripps Research—with creating a pipeline of talent and collaboration. “San Diego is one of the world-leading centers for technology, genomics, and RNA therapeutics,” she says. “We have over 30 RNA therapeutics companies here, and we support each other and help with anything related to drug discovery.”

She says that collaborative spirit extends beyond formal partnerships. “You can walk around Torrey Pines, go into a café, and find colleagues from the industry and have an ad hoc conversation,” Grossman says. “That’s something very unique to San Diego.”

While Snake Oil Venue Company may not be a household name, chances are many San Diegans have attended one of its events. The early-stage innovator honoree has expanded from beverage catering and mixology consulting into venue management, operating Julep Venue in Mission Hills, Bramble Bay Venue in Imperial Beach, Vesper Venue, the Chapel at Liberty Station, and five outdoor venues throughout Liberty Station—more than 500,000 square feet of event space altogether.

“We do a lot of launch parties for corporations and new products,” says CEO Mike Esposito. “I really like working on the entrepreneur side of things, where new businesses are entering the San Diego market and looking to make a splash.”

Snake Oil has executed more than 16,000 events, employed more than 1,000 people, and partnered with more than 900 local vendors, including caterers, florists, photographers, entertainers, and other hospitality businesses. The company also works with many of San Diego’s nonprofits, museums, and cultural institutions. “We get to celebrate people’s most important moments,” Esposito says. “Whether that’s a wedding, celebration of life, or quinceañera, we’re fortunate to be involved in the community in so many different ways.”

Photo Credit: Matt Furman

Growing a Beach-Town Brand into a National Business

Rising star honoree ALOHA Collection is proof that a simple idea can grow into a thriving company. Founded by two roommates who wanted a better way to carry wet swimsuits after a day at the beach, the lifestyle brand has grown into a business while maintaining strong year-over-year growth.

Now headquartered in Carlsbad, ALOHA Collection employs more than 100 people and operates its California flagship store in Encinitas, which is slated for a remodel. With roots in Hawaii, the company is known for its lightweight, splash-proof travel bags that have become a familiar sight on beaches in San Diego and beyond.

“‘Aloha’ is part of our name, but it’s also how we move through the world,” says CEO Lynna Barnard. “It’s how we show up for people, the way we travel, the way we give back.” Since day one, the company has maintained a 5 percent giveback to Hawaii conservation efforts, contributing millions of dollars over the years.

“I think what’s so inspiring about ALOHA Collection, and the founders in particular, is when you dream big, those dreams can come true when you work hard and trust in the universe,” Barnard says. “It’s inspiring to be a role model for other people wanting to start businesses from humble beginnings. Start small and watch it grow.”

Together, businesses like these form a cornerstone of San Diego’s economy—not only through the jobs and revenue they generate—but through the local workers they hire, vendors they support, and investments they make in the region. Their growth doesn’t happen in isolation; it ripples outward, strengthening the broader business community and the people who call San Diego home.

You don’t have to go far to get your forest fix in San Diego County—just take the 8 East past El Cajon and gain altitude in the Cuyamaca Mountains and you’ll hit Alpine, a quasi-rural community of 15,000 with sweeping views. Surrounded by national forest land and two reservations and perched at 2,000-feet elevation, Alpine is only about 30 miles east of downtown San Diego, perfect for a day trip when you’re in the mood for a small-town outing (or a stop along the way to the desert or Viejas).

The Kumeyaay hunted, gathered, and farmed in what is now Alpine more than 12,000 years ago before Spanish missionaries forced them to convert their villages to rancherias. By the late 1840s, after California and Mexico declared independence from Spain, the rancherias were consolidated into one massive “rancho,” and, in the 1850s, the area became a stopover on the “Jackass Mail,” SoCal’s first regular postal route. Then came the Gold Rush and a road to Julian, followed by another kind of gold: Alpine was California’s leading producer of honey in the late 1800s.

Former historical society president and honorary mayor Bob Ring says that during WWI, Alpine became known for having the “best climate” in the United States—healthy for soldiers’ convalescence or those with respiratory issues. Good weather, agriculture, and deer hunting brought folks to Alpine as it grew from hunting shacks to cottages to family homes.

Nowadays, Alpine is a place where “you have to get in touch with nature—because we have no movie theaters,” jokes real estate broker and former chamber of commerce board member Jeff Campbell, a resident since 1974. Getting outdoors in Alpine might mean joining 4-H or Future Farmers of America; hiking or dog-walking at Wright’s Field or Loveland Reservoir; riding horses, ATVs, and mountain bikes; or hitting the trails to discover seasonal waterfalls like Cedar Creek Falls, which cascades into a swimmable pool. Alpine is also the place to get up close with raptors at Sky Falconry and meet rescued big cats at the animal sanctuary Lions Tigers and Bears.

Photo Credit: Ariana Drehsler

Facts About Alpine, CA

Famous Broadway actor William Dalton, who went by the stage name Julian Eltinge and made a fortune playing women’s roles on stage, lived in Alpine in the 1920s. His ranch home still stands.

One of California’s earliest female physicians, Dr. Sophronia Nichols, lived in Alpine. Her 1896 home now houses the Alpine Historical Society Museum.

Former major league pitcher and Padres commentator Mark “Mud” Grant resides in Alpine.

Zillow reports the median home price in Alpine is almost $930,000.

Alpine has hosted its holiday Parade of Lights for 30 years. Thousands attend from all over San Diego County.

Photo Credit: Ariana Drehsler

The Locals’ Guide to Alpine, CA

“Here’s how favorites work in Alpine: We all have our preferred menu items at each of our town’s 11 eateries,” Campbell explains. The restaurants are mostly concentrated along Alpine Boulevard right off the 8.

Ring likes the rolled tacos at family-owned Alpine Taco Shop, with extra guac and cheese, while Campbell is partial to the fried fish tacos at Casino Inn Bar & Grill. According to Campbell, Franca’s Italian Kitchen and Bar has the best baked rigatoni not only in Alpine but in all of San Diego County. Ring goes there for family dinners and says he could be satisfied with “just the homemade bread with balsamic and olive oil.” Or head to Mediterraneo (locals call it “the Med”) for vegetarian lasagna. “I’m a keto dude, but it’s that good,” Campbell says.

For coffee, there’s The Well Cafe, where Cecilia Kennedy runs the shop and her husband Alan roasts beans in micro batches at home. Try the dark roast for drip and Mexican mocha for something a little fancier. Breakfast is a must at Janet’s Montana Cafe, which Campbell says serves the fluffiest pancakes, with no syrup needed. “[Janet’s has] homemade everything,” Ring adds, “but try the pies.” Grab supersized treats at Steph’s Donut Hole, and lunch is on the go at Barons Market, where you can pick up soup and salad.

Photo Credit: Ariana Drehsler

With two award-winning breweries in town, Alpine has a good beer scene for its size. Campbell gets the Assaulted By Feather Pillows IPA at Mike Hess Brewing and the Apricot Bells Bluff blonde ale at Mcilhenney Brewing Co.

The town also has a healthy populace of gearheads: Locals like to bring out their classic cars, motorcycles, dune buggies, and fifth wheels. Hang out on a Sunday to ogle old Thunderbirds, Mustangs, and Corvettes. For fun, Alpine parents take their kids to Viejas Outlet Center for outdoor ice skating in winter (and roller skating the rest of the year) or games at the center’s big arcade.

Overall, Campbell and Ring agree, you gotta have humor and heart to live in Alpine. “The culture of this community is that people are always willing to help, even in these busy times,” Ring says.

Photo Credit: Ariana Drehsler

What’s About to Happen?

Change in Alpine is incremental. Campbell anticipates Alpine’s mix of historic and suburban-type housing won’t shift dramatically in the near future, but he has seen some movement by the county to rezone some of its land to encourage more affordable units. “It’s my greatest hope for Alpine,” he says. “Nothing is deeded yet, but it’s on the county’s radar.”

Caltrans is also paying attention to the area, with a recent freeway expansion east of Alpine to Pine Valley, which means more road enhancements could be coming to the two-lane stretch of the 8 that leads from El Cajon west to Alpine.

A new state law that took effect in 2026 will certainly bring changes to Alpine’s mountain aesthetic: Homeowners and businesses must remove all combustible materials within five feet of any structure to help prevent fires. Compliance means replacement of existing landscaping with bare soil, rocks, gravel, concrete, or stone. It could be a whole different look for a rugged town with natural smatterings of oaks, bushy sage, and chaparral.

Campbell has recently seen positive growth and possible expansion in the tribal areas, with new housing subdivisions. In Alpine, he’s noticed a gradual ADU trend, gaining momentum but not catching on as quickly as in other parts of San Diego—“because people come out here for elbow room,” he says.

It’s kind of big news that there’s talk of a small grocery store incoming (the first supermarket to arrive in town since Barons in 2015). New businesses in Alpine used to be heralded with ribbon-cuttings by the chamber of commerce, which disbanded last year—but, Campbell has heard, the organization may get revived soon and bring back this charmingly small-town style of welcome. “Alpine has a need for a center to elevate business to a new level,” he says.

Need help deciding which of La Jolla’s seemingly endless beaches to lay your towel out at today? Each little sandy sliver between the neighborhood’s sea cliffs has its own name and character: the Cove for swimming, Children’s Pool for seal-watching, Wipeout Beach for skim-boarding. Head to La Jolla Shores for that wide, sandy, picnic-with-the-family feel, and if you know what you’re doing, go surfing at Windansea or Bird Rock (if you’re a beginner, opt instead for the Shores, where most of San Diego learned to surf).

Of course, beachy isn’t La Jolla’s only vibe. The Village (locals don’t call it downtown anymore, says La Jolla resident and senior editor of lajolla.ca Elisabeth Frausto) is La Jolla’s most walkable area—highlighted by the main drag, Prospect Street—with a wide radius of shop-lined roads sloping down to the coast.

At long standing neighborhood staples like Warwick’s bookstore and Harry’s Coffee Shop, “old-timers still belly up to the counter and talk politics,” Frausto says. Art enthusiasts visit to peruse through its many galleries, including Quint and Joseph Bellows, and check out what’s on at the Museum of Contemporary Art San Diego (MCASD). Shoppers wander Girard Avenue, picking out activewear at Lululemon and Vuori and fancier digs at Thread + Seed and Sigi’s Boutique. Friends gossip and sip coffee at locally owned outposts like Flower Pot Cafe and Il Giardino Di Lilli.

Courtesy of Il Giardino Di Lilli

Once isolated from the rest of San Diego, La Jolla became a popular resort destination when the San Diego, Pacific Beach, and La Jolla Railway arrived in the 1890s and made the area more accessible to visitors (who wanted to spend time there so badly they stayed in tents during the summer). Some of those tourists got creative, too.

“Our tradition of supporting the arts goes back to the days of the Green Dragon Artist Colony that was founded in 1894,” says Athenaeum Music & Arts Library Executive Director Christie Mitchell. Anna Held started the Green Dragon Colony to attract visiting artists to La Jolla for a weekend getaway; it quickly became a venue for ad-hoc performances and bohemian artists’ salons.

However, it was Ellen Browning Scripps more than anyone who shaped La Jolla into the neighborhood we know today, commissioning buildings like the structure that now houses MCASD. The arrival of the Scripps Institution of Oceanography in 1907 laid the foundation for the establishment of UC San Diego 53 years later at the longtime site of the military base Camp Matthews. All of these developments helped establish La Jolla’s layered identities: high-dollar beach town, arts magnet, academic research hub.

Photo Credit: Ariana Drehsler

Facts About La Jolla, CA

Ellen Browning Scripps commissioned Irving Gill to design a building for the La Jolla Woman’s Club in 1914; it still meets today in the same building.

La Jolla’s scenic beauty is a backdrop for many movies, including Thor, Gattaca, Traffic, Mr. Jones, and Andy Warhol’s 1968 experimental film San Diego Surf.

Every summer, thousands of pregnant female leopard sharks gather in La Jolla’s Marine Protected Areas to incubate their pups.

Zillow reports the average home price in La Jolla is $2.3 million.

Old Hollywood film star and La Jolla native Gregory Peck was one of the founders of La Jolla Playhouse, which opened its doors in 1947.

Photo Credit: Ariana Drehsler

Locals’ Guide to La Jolla, CA

Athenaeum Music & Arts Director Christie Mitchell is a bona fide La Jolla local, having grown up in the LJ neighborhood of Bird Rock. Her dad still surfs, and Mitchell met her own surfer husband at La Jolla High (their toddler has already tried surfing, too). Mitchell’s mom still lives in Bird Rock, and “it’s gotten a lot livelier and more pedestrian-friendly,” she says.

On weekends, she makes sure to hit Wayfarer Bread for “the gooiest, heaviest, stickiest cinnamon loaf—definitely preorder because there’s always a line,” she advises. Friday and Saturday are pizza night at Wayfarer, and the bakery’s industry collabs produce some unique pies. For coffee, head to Bird Rock Coffee Roasters, of course, where you can grab a cup and hang out in the open-air seating or stroll to La Jolla Hermosa Park for ocean views (and a skate park and bike paths for little ones to tire themselves out on).

One of Mitchell’s favorites for lunch with coworkers in the Village is Peruvian-inspired Pepino, owned by one of her high school classmates. “The sweet potato bowl is really good,” she says.

Courtesy of The Marine Room

She also cherishes La Jolla institutions. The Ascot Shop, a longtime men’s clothing boutique, is a go-to for gifts; founded by a local fisherman, El Pescador Fish Market is the place for the freshest seafood and fish tacos; and The Marine Room is for special occasions, with on-point service against a backdrop of crashing waves. “And nothing says ‘La Jolla’ like George’s at the Cove,” Mitchell adds. “With the John Baldessari mural and the view, it’s a great mix of the arts and the ocean.”

There’s a surprising amount to do on the weekdays in La Jolla, Mitchell says, with free live music every Monday at the Athenaeum (and weekly ticketed events), late-night DJ sessions at Le Coq, acts at The Comedy Store, concerts at the The Conrad (home of La Jolla Music Society), and the monthly First Friday Art Walk.

Photo Credit: Kimberly Motos

What’s About to Happen

The biggest talk of the town for La Jollans? Possible secession from the city of San Diego, Frausto says. Proponents want to separate so La Jolla can maintain its own infrastructure and make decisions about development (critics say La Jolla should contribute taxes to the rest of the city). If the initiative advances, final say would come down to a city-wide vote.

Additionally, locals and visitors alike are witnessing a genuine culinary explosion. Restaurateur Sami Ladeki’s Roppongi, a Japanese fusion and sushi favorite that closed in 2015, reopened in December 2025 under returning chef Alfie Szeprethy. Michelin-starred chef Elijah Arizmendi launched tasting-menu-only restaurant Lucien last year, and chef Accursio Lota of North Park’s Cori Trattoria Pastifico opened his new spot Dora in November. Local designers Paul Basile and Jules Wilson are building Roseacre, 5,000 square feet of culinary concepts on Girard Avenue. And one of La Jolla’s favorite restaurant families is opening a completely new eatery near Torrey Pines Golf Course in summer 2026: From the guys behind Puesto and Marisi comes an Eastern Mediterranean spot called Ikaria.

Back in the Village, a new boutique hotel by Orli is landing in the old nurses’ quarters (now condos) next to the original 1924 Scripps hospital (the institution moved to Genesee Avenue in 1964). La Jolla is also getting in on the thrifting trend—Goodwill opened a shop on Herschel Avenue in early 2026.

Pedestrian-friendly changes are afoot in two of LJ’s walkable areas. At La Jolla Shores, look for enhancements to Avenida de la Playa from El Paseo Grande to Calle de la Plata, where the street has been closed to vehicles since 2020 for outdoor dining. The Village Streetscape Plan is coming to Girard Avenue between Silverado Street and Prospect Street, bringing expanded walking areas, corner parks, improved lighting, new seating, public art, and landscaping to create shade canopies and gathering spaces.

Photo Credit: Ariana Drehsler

Also look for beautification projects along the coast. The 1920s stairs leading down to the tide pools at Whale View Point are finally getting a redo; Ellen Browning Scripps Park will receive fresh sod and much-needed widened sidewalks. And ADA trail improvements and a new restroom facility are on their way at Torrey Pines State Natural Reserve, making the beloved natural area more accessible.

As for housing, Frausto says, affordable units are hard to come by, and that probably won’t change soon. Most new homes and apartments are geared toward the luxury market, like La Jolla’s first new gated community in 40 years, Foxhill, which broke ground in October 2025 on the site of a former golf course—with empty lots selling for more than $8 million.

It’s estimated that 44% of women in the U.S. have high blood pressure, also known as hypertension, but many don’t know it. The disease often has no symptoms, and when symptoms do present, they can appear similar to many other conditions. High blood pressure increases the risk for heart disease and stroke, so it’s critical that it’s detected and treated early. And for women at risk of developing high blood pressure, prevention is key. Click here for the basics of high blood pressure and how Scripps physicians at Scripps use screenings not just as a diagnostic tool, but as part of routine preventive care.

For more nutrition, wellness, and healthy living tips, sign up for the San Diego Health newsletter here.